The 'Frenemy' Dynamic: NVIDIA, OpenAI, and Oracle in the Evolving AI Landscape

Analyzing NVIDIA's Q3 fiscal 2026 earnings, this article explores potential financial concerns amidst record revenue. It delves into 'circular financing' theories involving OpenAI and Oracle, OpenAI's strategic moves to lessen NVIDIA dependency, and Oracle's compelling case for acquiring Groq to secure its position in the competitive AI hardware market.

NVIDIA's Complex Relationships with OpenAI and Oracle

NVIDIA's Q3 Fiscal 2026 earnings report initially presents a picture of robust growth, with revenue up 62% to $57 billion and CEO Jensen Huang highlighting a "virtuous cycle of AI." However, a deeper analysis of the financial statements, cross-referenced with recent developments involving OpenAI and Oracle, suggests potential underlying tensions within the "AI Alliance." While NVIDIA achieves record numbers, its major customers appear to be strategically positioning themselves for increased independence.

This analysis will explore the dynamics of the AI hardware market, the "frenemy" relationship between OpenAI and NVIDIA, and the "circular financing" theories that have garnered attention from financial observers like Michael Burry.

Key areas of discussion include:

- NVIDIA's Earnings: Strengths and areas of concern

- Interpreting 'Round-Tripping' financial reports

- OpenAI's initiatives to reduce NVIDIA dependency

- Oracle's strategic opportunity: The Groq acquisition

- Concluding thoughts on the market's future

NVIDIA's Earnings: Perfection with Underlying Stress

Superficially, NVIDIA stands as a dominant force in the AI era, with its Data Center segment now comprising nearly 90% of the company's business. Yet, a closer examination of the financials reveals three specific points warranting scrutiny:

- The Cash Flow Discrepancy: NVIDIA reported a substantial $31.9 billion in Net Income, but only generated $23.8 billion in Operating Cash Flow. This $8 billion difference indicates a delay in converting profits directly into cash.

- Inventory Expansion: Inventory levels have almost doubled this year, reaching $19.8 billion. While management attributes this to preparations for the 'Blackwell' launch, holding approximately 120 days of inventory represents a significant capital drag.

- Extended Payment Cycles: The Days Sales Outstanding (DSO) has increased to about 53 days. As revenue rapidly escalates, NVIDIA is waiting nearly two months for payments, which could suggest extended credit terms offered to enterprise clients to sustain market momentum.

These indicators suggest NVIDIA is making substantial upfront investments in inventory, anticipating rapid sales of its Blackwell architecture in Q4.

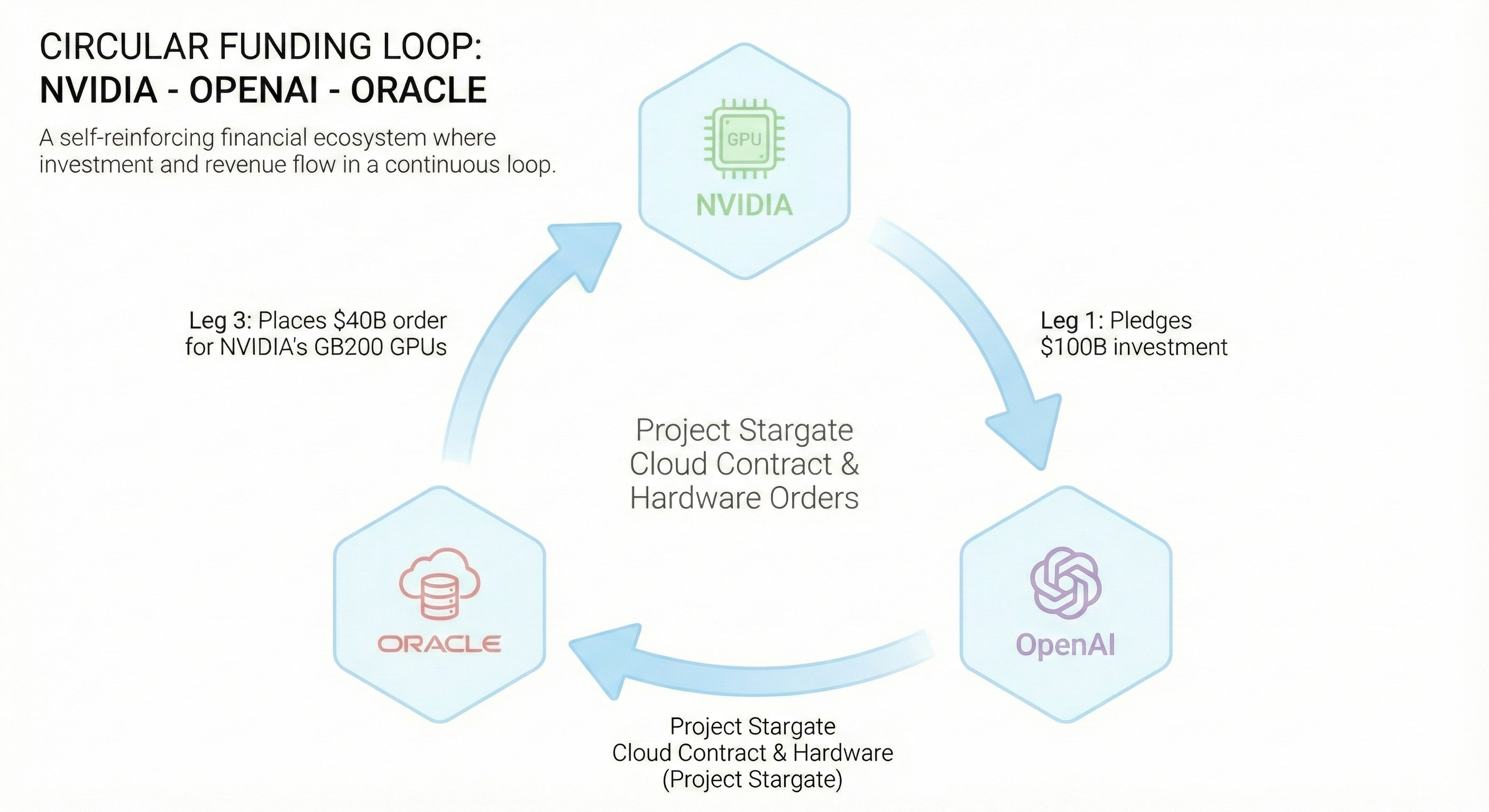

Making Sense of 'Round-Tripping' News

Recent financial news, amplified by figures such as Michael Burry, has highlighted concerns about 'circular financing' and potentially questionable revenue recognition practices. This involves a complex web of deals that can be visualized as follows:

- Leg 1: NVIDIA commits billions (part of a reported $100 billion investment roadmap) to OpenAI.

- Leg 2: OpenAI secures a significant $300 billion cloud contract with Oracle (Project Stargate) for hosting its models.

- Leg 3: To fulfill this contract, Oracle then places a $40 billion order for NVIDIA’s GB200 GPUs.

Burry's argument, which is reportedly under review by regulators like the DOJ, suggests that this structure mimics 'round-tripping.' It raises a critical question: Would OpenAI possess the necessary capital for its Oracle deal, and would Oracle proceed with its chip orders, if NVIDIA ceased its investments in OpenAI? A negative answer would imply a more fragile revenue stream than initially perceived.

OpenAI's Strategic Moves to Reduce NVIDIA Dependency

OpenAI, once a primary partner for NVIDIA, increasingly appears to be developing capabilities that could position it as a future competitor. While currently collaborating closely with NVIDIA for massive infrastructure deployments, evidence suggests OpenAI is simultaneously building an independent supply chain.

'Project Stargate' is not merely a data center; it represents an extensive infrastructure plan encompassing custom hardware. OpenAI has reportedly bypassed NVIDIA's supply chain by directly procuring DRAM wafers from major HBM providers Samsung and SK Hynix, a move widely reported and debated within the industry.

Furthermore, talent acquisition points to this strategic shift: OpenAI has recruited key silicon talent, including Richard Ho (formerly Google’s TPU lead) in 2023, and approximately 40 hardware engineers from Apple more recently.

In partnership with Broadcom, OpenAI is speculated to use NVIDIA GPUs for intelligence creation while leveraging its own custom silicon, or potentially Edge TPU-like chips, for inference to optimize costs—a strategy akin to Google's NPU chips. Critical questions remain regarding OpenAI's funding for these initiatives and NVIDIA's potential influence over OpenAI's future hardware plans, particularly given the unconfirmed $100 billion NVIDIA investment.

Oracle's Strategic Opportunity: The Groq Acquisition

The rising costs associated with AI inference—the expense of running LLMs like ChatGPT versus training them—are a significant industry concern. Groq, a startup founded by Jonathan Ross (a former Google TPU lead and innovator behind the TPU concept), claims to offer faster and more cost-effective solutions for inference compared to NVIDIA.

An additional factor often overlooked is the current HBM (High Bandwidth Memory) shortage, which significantly constrains NVIDIA's supply chain due to overwhelmed specialized memory fabs. Groq's architecture, however, relies on SRAM (Static RAM), which is typically manufactured in logic fabs alongside processors, potentially circumventing the HBM supply crunch.

Considering these factors, Oracle could benefit significantly from acquiring Groq. Such an acquisition would not only provide Oracle with a faster inference chip but also a potentially more readily available one amidst widespread component shortages—serving as a crucial supply chain hedge. This would also offer a massive advantage to its primary client, OpenAI, enabling faster and cheaper inference capabilities.

Given that Oracle's margins on renting NVIDIA chips are reportedly as low as 14%, acquiring Groq would allow Oracle to bypass the 'NVIDIA Tax,' improve its margins, and mitigate the HBM shortage. With Groq valued at approximately $6.9 billion as of its September 2025 funding round, Oracle possesses the financial capacity for such an acquisition.

However, this scenario prompts further questions about NVIDIA's reaction. Would NVIDIA permit such a deal, and if not, what implications would that have for the 'circular funding' arrangements? Could an unstated quid pro quo exist, where NVIDIA's investments in OpenAI are linked to Oracle's exclusive reliance on NVIDIA hardware?

Final Thoughts

As 2026 unfolds, the dynamics between NVIDIA, OpenAI, and Oracle appear increasingly intertwined and competitive. Key uncertainties persist: Did NVIDIA have prior knowledge of OpenAI's direct wafer memory supply deals? Is NVIDIA actively striving for exclusivity in both training and inference at Project Stargate? What specific chip architectures—such as TPU/LPU-like or Edge TPU—is OpenAI planning to develop?

The AI hardware market remains exceptionally dynamic, and the coming quarters are anticipated to reveal significant strategic shifts. Notably, Google has reportedly responded to the memory wafer shortage by securing a major deal with Samsung for 2026, indicating broader industry efforts to manage supply chain risks.